Apartments and townhouses in Coombs. With few affordable standalone houses available, buyers are adjusting their expectations. Photo: Michelle Kroll.

Canberra house prices continued their upward march in August, leading the nation as stock dwindles due to a combination of the usual winter slowdown and the fallout from the COVID-19 pandemic.

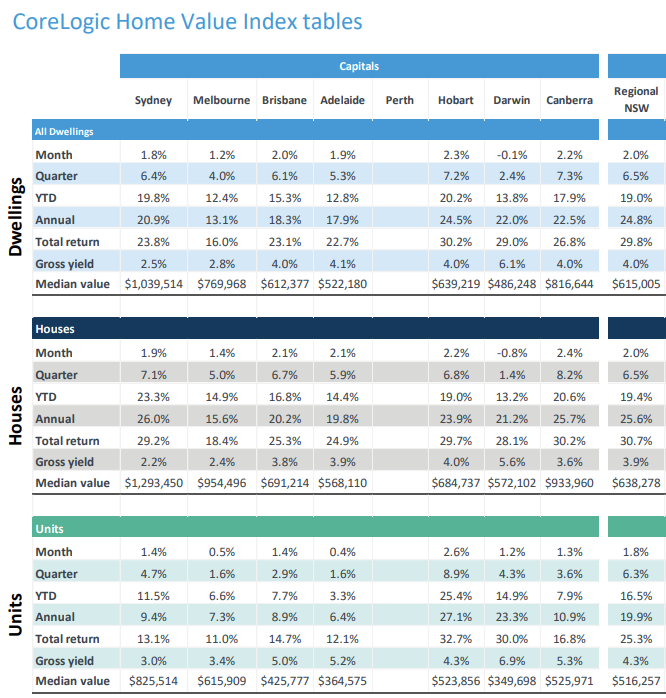

The latest data from CoreLogic shows the median standalone house price is now heading towards $950,000 and closing in on Melbourne, after a 2.4 per cent rise that takes the overall increase so far this year to a whopping 20.6 per cent and 25.7 per cent over the past 12 months.

That’s less than July’s 3 per cent jump, but it may be due to a dwindling of supply and buyers moving into the much cheaper townhouse and unit market where prices increased another 1.3 per cent, sustaining the previous month’s growth.

Overall, Canberra home prices rose 2.2 per cent, just behind leader Hobart at 2.3 per cent.

Last weekend only 37 homes – 27 houses (reported), four townhouses and four units – sold, from a scheduled listing of 85, with 46 reported, for a still high clearance rate of 80.4 per cent, where Canberra auction sales have been hovering for some time.

Note: The figures for Perth and WA have been temporarily withdrawn while divergence from other housing market measurements is being checked. Image: CoreLogic.

The median price was $877,500. A two-bedroom house in Euree Street, Reid, on a huge inner-city block of 1045 square metres, lead the pack, selling for $2,025,000. The weekend before, a Yarralumla property in Musgrave Street sold for more than $3 million.

All of the top 10 sold for $1 million or more and 20 sold before auction, showing demand remains super strong.

The hopeful release from lockdown in mid-September and the traditional spring selling season may lift listings out of the doldrums.

According to SQM Research, Canberra listings in August were down 36.5 per cent from last year, dropping from 3902 to 2478. In July, in the depths of winter, there were 3035 listings.

With few houses to choose from, buyers are adjusting their expectations and looking at the townhouse and unit market where there are more properties in their price range.

That is helping to boost those prices, with the median now at nearly $526,000, the third-highest in the nation behind Sydney and Melbourne.

The 1.3 per cent increase was just behind Sydney and Brisbane at 1.4 per cent, and meant unit and townhouse prices have picked up steam this year with an almost 8 per cent rise, compared to the 12-month increase of nearly 11 per cent.

With its high average incomes, Canberra is not experiencing the moderating of prices evident in the national figure of a 1.5 per cent rise in August, which is still contributing to the fastest annual pace of growth in housing values for 32 years.

CoreLogic research director Tim Lawless says the slowing growth rate probably has more to do with worsening affordability than ongoing lockdowns.

“Housing prices have risen almost 11 times faster than wages growth over the past year, creating a more significant barrier to entry for those who don’t yet own a home,” he said.

“Lockdowns are having a clear impact on consumer sentiment; however, to date, the restrictions have resulted in falling advertised listings and, to a lesser extent, fewer home sales, with less impact on price growth momentum.

“It’s likely the ongoing shortage of properties available for purchase is central to the upwards pressure on housing values.”

Capital city house prices continue to grow more strongly than units, although the gap appears to be narrowing, which Mr Lawless says could be another sign that affordability is becoming more challenging.